Conversion Settlement

8 July 2020

Historically, traditional convertible securities had been settled with underlying shares upon their conversion. However, over the last several years, there has been a significant shift globally towards a full or partial settlement of the conversion rights in cash.

Having been introduced in the US market a couple of decades ago to manage financial accounting and to provide financial flexibility to the issuers in general, this feature has grown in popularity globally and has evolved through multiple iterations. Several common conventions have become established to fit the various regional markets' issuer needs and investor expectations.

Prevalent feature in the US

In the US, partial cash (so-called "flexible", or "net-share") conversion settlement has turned into the norm rather than the exception and has become quite standardized in its setup. In fact, 82% of the convertible securities (excluding PEPS or mandatory preferred structures) currently comprising the outstanding US universe in the Monis Data Service (MDS), have been issued with either a flexible or full cash conversion settlement feature. The feature’s prevalence has also been increasing more recently: in the last 5 years, 85% of issues, and in the last year almost 90% of issues, have flexible conversion settlement.

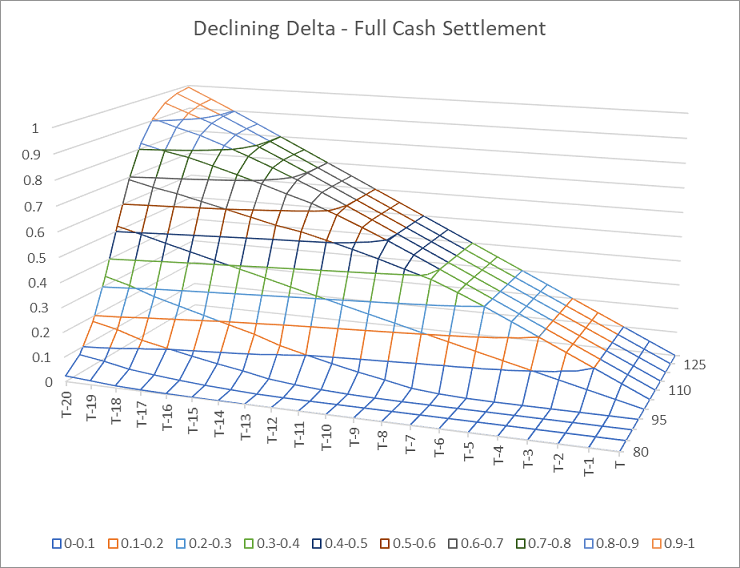

Despite the overall standardization of the conversion settlement language among US convertible bonds, there remains quite a lot of variability in the length of the "observation", or averaging, period embedded in this feature. While 40 trading days is the most common averaging period (just over 40% of cash-settleable convertibles), it ranges from 1 to 100 trading days; 20, 30 and 50 trading day periods are the next most common. The longer the conversion settlement averaging period, the more significant its impact on the convertible valuation and greeks, especially delta. Significantly, averaging periods more often tend to run before the relevant maturity or redemption date meaning the real conversion value is known, or at least close to being known, before the conversion decision must be taken.

Europe and Asia

The feature is not so prevalent in Europe and Asia, with only around a half of European issues and around a quarter of Asian issues having some form of cash conversion settlement. It is also less homogenous; for some issues it may only be applied in exceptional circumstances (in which case MDS pre-populates the necessary fields but does not activate the feature), some European issues (around 15%) are solely cash settled and Japanese issues with this feature tend to only apply it for conversion upon acquisition. It is quite common in both Europe and Asia for the default settlement to be all shares, but for the issuer to have the option to elect otherwise, after the conversion decision has been taken. Hence, it is quite common for the averaging period to be based off this issuer election notice. Averaging periods vary between 1 to 50 trading days in Europe and 3 to 90 trading days in Asia, with 20 days being the most common in both regions (around 40% of issues).

Valuation in the Convertible Model

The cash or combination "conversion" value delivered to holders is intended to replicate closely the value of receiving actual shares. However, using averaging implies that—particularly once averaging has already begun—the expected conversion value can start to diverge from the value of the physical shares. This impact can become quite pronounced for longer averaging periods.

There are two particularly important examples which may have a significant impact on the valuation.

- The first, and more common, is when the averaging, or Observation Period for the share price is set to begin some number of days prior to the bond maturity date. However, conversion rights may not expire until mid-way through or after this Observation Period. This means that the value of conversion starts to crystallize as the final conversion date approaches and, importantly, becomes less dependent on the actual prevailing share price. This implies a gradual reduction in Delta over the course of the Observation Period, and hence a gradual unwinding of the hedge position.

- The second exists when the Observation Period is defined with reference to a call redemption date, and the stipulation is such that an issuer's minimum notice requirements imply an Observation Period which could start prior to the date on which the call notice needs to be given. This means that past share prices can become important in evaluating the value of the call option due to the impact on the projected value of a call-forced conversion.

The Monis conversion settlement feature supports these and other examples using a grid of "Settlement Periods' data. If conversion notice is given on a date within a particular conversion Settlement Period, then the payoff is assumed to be subject to an averaging "Observation Period" which determines the quantities of cash and shares to be received and therefore the "value" of converting.

Further explanation of our valuation approach for the feature can be found in the Monis Convertible Bond White Paper, an excerpt of which is copied at the end of this report.

Delta impact

Typically, in-the-money convertibles exhibit a gradually rising delta as the instrument approaches conversion expiry (either at maturity or in relation to an early redemption), ceteris paribus. However, this assumes holders receive the underlying shares on conversion. Thus, typical hedging requires selling an increasing number of shares to match the increasing delta, so that shares received on conversion may be delivered to close out the short position entirely.

In the case of full cash settlement, the opposite is true; delta declines through the averaging period as the cash “conversion” value crystallizes, to the point where this becomes entirely independent of the underlying share price. The hedging strategy in this case requires a gradual buying back of the short position in the underlying shares, with traders attempting to match the decreasing delta through the averaging period.

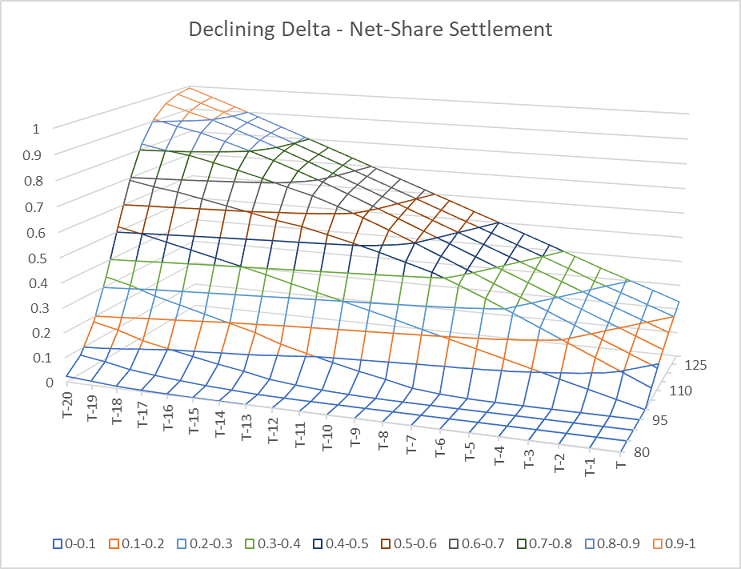

For net-share settlement, as expected we observe a combination of these two extremes. The instrument delta becomes dependent on the “new ratio” of top-up shares that will be received in addition to the cash value. In this case, holders of a hedged position will still be attempting to match the delta through the averaging period but may require buying or selling shares in order that the short position matches the number of top-up shares resulting at the end of the averaging period.

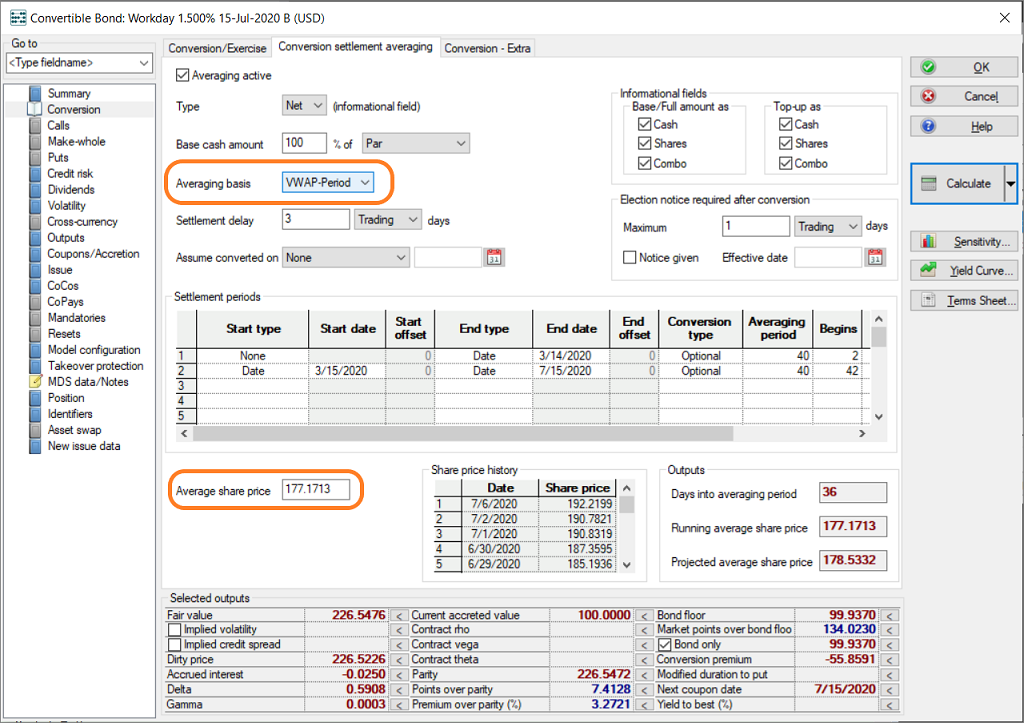

Conversion Settlement setup on the instrument GUI

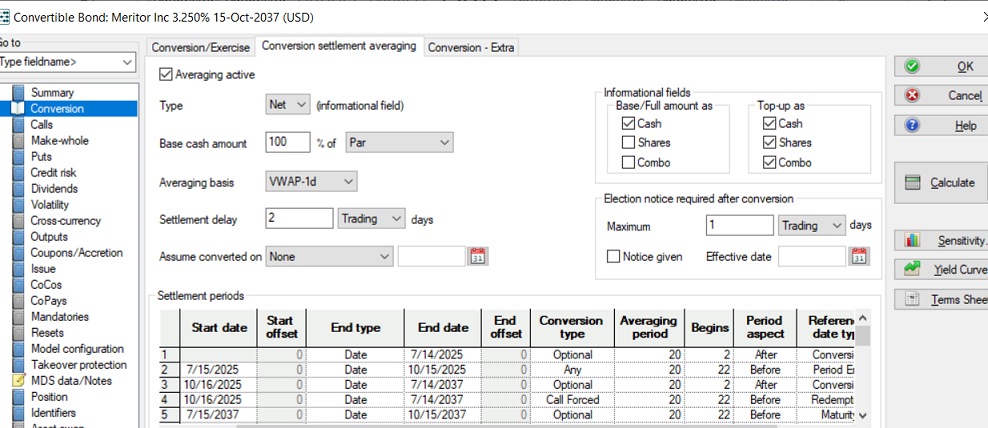

To handle the flexible/cash conversion settlement feature in the model, all Monis products now include a Conversion settlement averaging tab in the Conversion section of the instrument GUI (see below), with structural complexities captured by the Settlement Periods grid. The grid can handle all Settlement Periods, whether conversion is optional, call-forced or at maturity, as exemplified by Meritor 3.25% 2037. Correctly setting the "Base cash amount", representing the portion of cash that holders expect to receive on conversion, is important to the valuation: this would typically be set as 100% of "Parity Value" (for full cash settlement) or 100% of "Par" (for partial, or net-share, settlement.) N.B., setting the "Type" dropdown to either Full or Net is purely informational and does not impact the valuation.

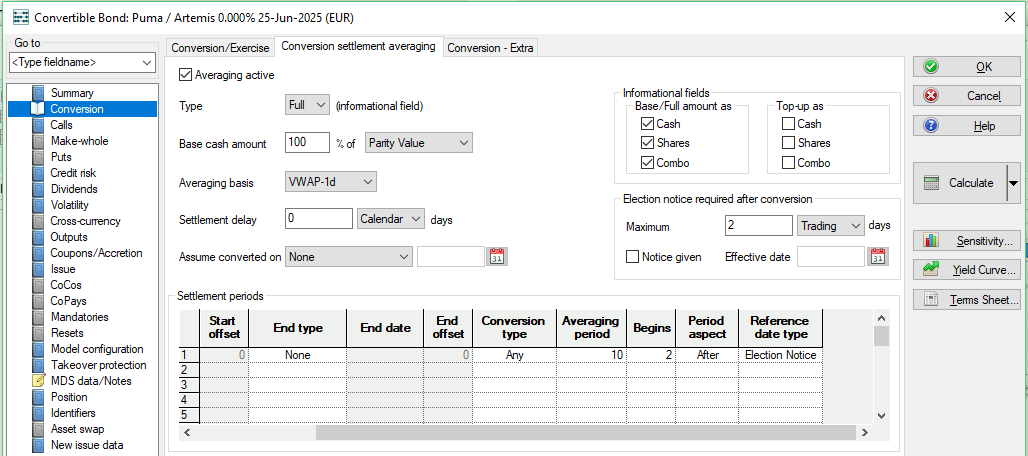

A common feature in Europe and Asia is for the issuer to be able to elect whether to deliver cash or a combination (with full share settlement often the default). In this case the averaging Observation Period references the issuer's Election Notice Date. In the example below, the issuer has 2 trading days after conversion notice has been given to decide the form of the conversion consideration. Therefore, in these cases the Notice given checkbox and Effective date both enable the feature and drive the settlement period determination.

MDS data coverage

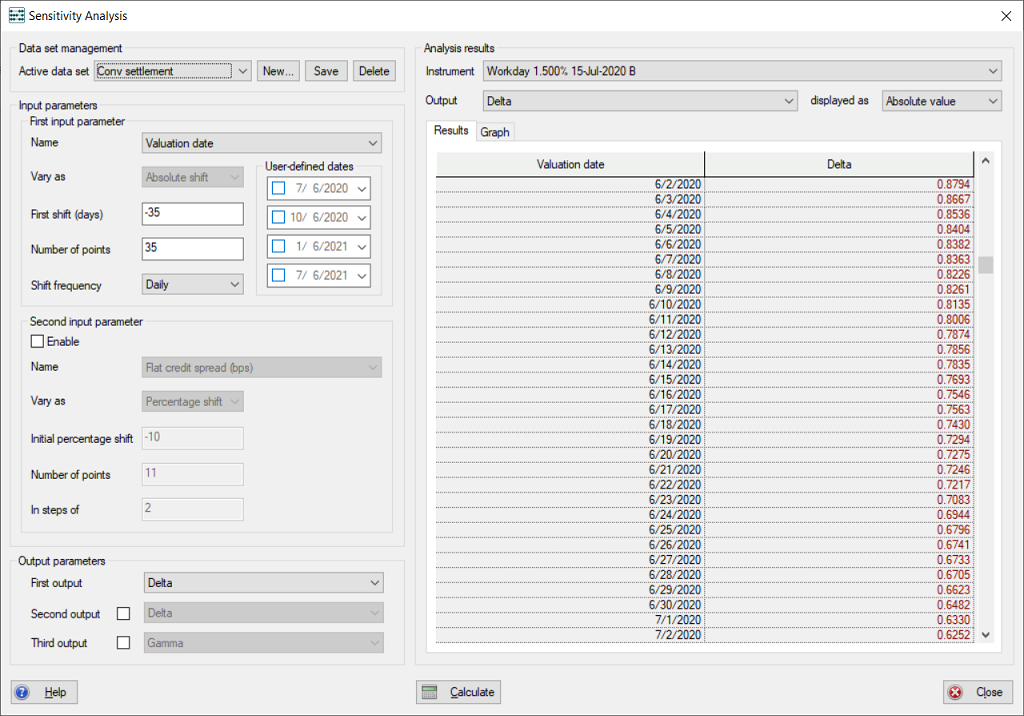

The Monis Data team has populated all the original terms and conditions details required to be able to use the feature immediately. In addition, MDS also captures important life-cycle fields for any "active" conversion settlement situations, for example the Workday 1.500% 15-Jul-2020 B convertible bond that is nearing its maturity - see table below for full details. As of 6-Jul-2020, it is 36 days into its 40-day averaging period and the Share price history grid captures the daily VWAP stock prices that have already occurred, resulting in the Running average share price over the period so far. The Projected average share price utilizes these already confirmed historical values and applies the latest share price to the remaining days in the averaging period.

The decreasing delta over the averaging period so far can be illustrated using the Sensitivity Analysis function of Monis, looking back to the start of the averaging period and up to today.

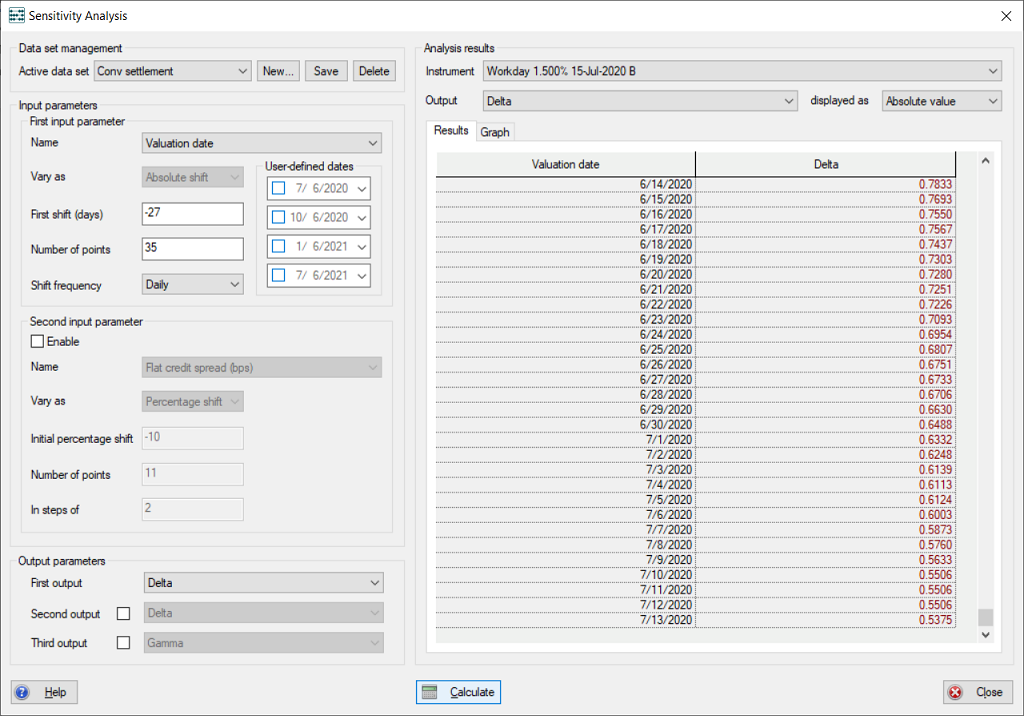

It might be considered a simple matter to run a forward sensitivity analysis by merely pushing the valuation date ahead in the sensitivity interface. However, the design of this initial release prioritizes the current running average and an expectation by the analytics of a fully populated averaging array means that a simplistic analysis will not result in the declining delta expected. So, in order to correctly run a forward-looking delta sensitivity analysis, the user should switch the averaging basis to VWAP-Period and simply populate the average share price with the current running average in order to save having to enter unknown future share prices manually, as per the example below.

The resultant forward Sensitivity analysis illustrates the gradual reduction of delta until the Last conversion date of 13-Jul-2020. As this bond is quite deep in-the-money and settles as a "net-share", i.e. the principal amount to be paid in cash and the remainder in shares, the share conversion value remains quite significant and explains the relatively high delta on the last day of the settlement period.

Convertibles within active conversion settlement periods

In the table below we highlight those convertibles that are currently within their respective averaging periods, along with details of the relevant averaging periods and key valuation outputs incorporating the conversion settlement cash averaging.

| Name | Observation Start | Observation End | Settlement Type | Averaging Period | Begins | Reference Type | Reference Date | Conversion Expires | Days Into Averaging | Running Avg Share Price | Projected Avg Share Price | FV | Parity | Delta |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Restoration Hardware (RH) 0.000% 15-Jul-2020 | 07-May-20 | 13-Jul-20 | NET | 45 | 47T BEFORE | MATURITY | 15-Jul-20 | 13-Jul-20 | 42 | 221.7 | 224.1 | 203.1 | 203.1 | 0.511 |

| Workday 1.500% 15-Jul-2020 B | 14-May-20 | 13-Jul-20 | NET | 40 | 42T BEFORE | MATURITY | 15-Jul-20 | 13-Jul-20 | 37 | 177.6 | 178.6 | 227.1 | 227.1 | 0.578 |

| DexCom 0.750% 15-May-2022 | 30-Jun-20 | 29-Jul-20 | NET | 20 | 22T BEFORE | REDEMPTION | 15-May-22 | 13-May-22 | 5 | 413.3 | 422.7 | 428.9 | 429.0 | 0.942 |

| Portfolio Recovery Associates 3.000% 01-Aug-2020 | 03-Jun-20 | 30-Jul-20 | NET | 40 | 42T BEFORE | MATURITY | 01-Aug-20 | 30-Jul-20 | 24 | 37.9 | 37.4 | 100.0 | 57.0 | 0.000 |

Contact us

If you would like to discuss this, or any other aspect of Monis or the Data Service, please feel free to contact us at Monis support.

Addendum

There follows below an excerpt from the Monis Convertible Bond White Paper, detailing our treatment of the conversion settlement feature.

5.11 Conversion settlement

Exercise of conversion rights does not always result in physical delivery of the underlying shares by the issuer, but instead conversion can be settled in cash or some combination of cash and shares. The cash or combination values delivered to the holder are intended to replicate closely the value of receiving actual shares but often involve the calculation of an average share price which is used to determine the cash amounts (and possibly top-up share amounts). The implication of this averaging is that, particularly once averaging has already begun, the expected cash and combination values can start to diverge from the value of the physical shares.

There are two particularly important examples which may have significant impact on valuation. The first, and more common, is when the averaging period for the share price (often referred to as the "Observation Period") is set to begin some number of days prior to the bond maturity date. However, conversion rights may not expire until mid-way through or after this Observation Period. This means the value of conversion starts to crystallize as the final conversion date approaches and, importantly, becomes less dependent on the actual prevailing share price. This implies a gradual reduction in Delta over the course of the Observation Period and hence a gradual unwinding of the hedge position.

The second important example exists when the Observation Period is defined with reference to a call redemption date and the stipulation is such that an issuer's minimum notice requirements imply an Observation Period which could start prior to the date where the call notice needs to be given. This means that past share prices can become important in evaluating the value of the call option due to the impact on the projected value of a call forced conversion.

5.11.1 Conversion settlement periods

The above examples, and others, are supported in Monis (with some simplifying assumptions for the averaging) and are specified as an array of "Settlement Periods". If conversion notice is given on a date within a Settlement Period, then the payoff is assumed to be subject to an averaging "Observation Period" which determines the quantities of cash and shares to be received and therefore the "value" of converting.

5.11.2 The observation period

Each "Settlement Period" defines exactly one Observation Period over which an average share price is computed. The Observation Period is defined by the number of trading days it comprises, and the number of trading days it commences before, or after, a reference date (which may be any of the Maturity Date, Conversion Date, Election Notice Date, Call Notice Date, Call Redemption Date or Settlement Period End Date.) Note that the Observation Period may or may not be fixed, depending on whether the reference date defining it is itself fixed (e.g. the Maturity Date) or unknown at present (e.g. a future Conversion Date). [The Election Notice Date is the date on which the issuer delivers an 'election notice' of its decision to exercise some form of cash settlement. This will typically occur in the days immediately following the Conversion Date.]

5.11.3 Conversion settlement payoff

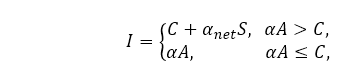

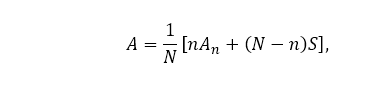

The value of full cash, combination (or "Net-share") and physical settlement can all be described in a generalised formula of the conversion payoff:

where:

In Monis the maximum cash amount C is specified as a percentage of some reference quantity, either Par, Parity or the Accreted Principal Amount (as of the Conversion Date). Modelling the possible future values of the average share price A presents a significant problem from a valuation perspective due to its dependence on the path the share price takes. A full treatment would require an additional pricing dimension or simulation, both of which would lead to serious degradation in calculation performance. So, a much simpler approach is taken, which is to calculate expected average share prices A (and therefore expected conversion payoffs). For each relevant Tree or PDE node we weight the known running average so far with the share price at that node according to:

where:

This method captures the important behaviour, a decreasing Delta over the Observation Period and convergence towards a payoff based on the average share price, without sacrificing performance.

philip.kramer@fisglobal.com

tatyana.hube@fisglobal.com

william.weichhart@fisglobal.com

monis.data@fisglobal.com

Copyright © 2020 by Fidelity National Information Services, Inc. and/or its subsidiaries ("FIS"). This document is copyrighted with all rights reserved. No part of this document may be reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of FIS. Except as set out in the contract your company has with FIS, in no event shall FIS be liable for damages of any kind arising out of the use of this document.