SPAC Warrants: Modelling the Soft-Call

10 June 2021

A Special Purpose Acquisition Company (SPAC), also known as a "blank cheque company", is a shell company created to identify and acquire a target company to take public. Whilst not a new idea, SPACs have experienced an explosive surge in popularity over the last 18 months as an alternative to the traditional IPO.

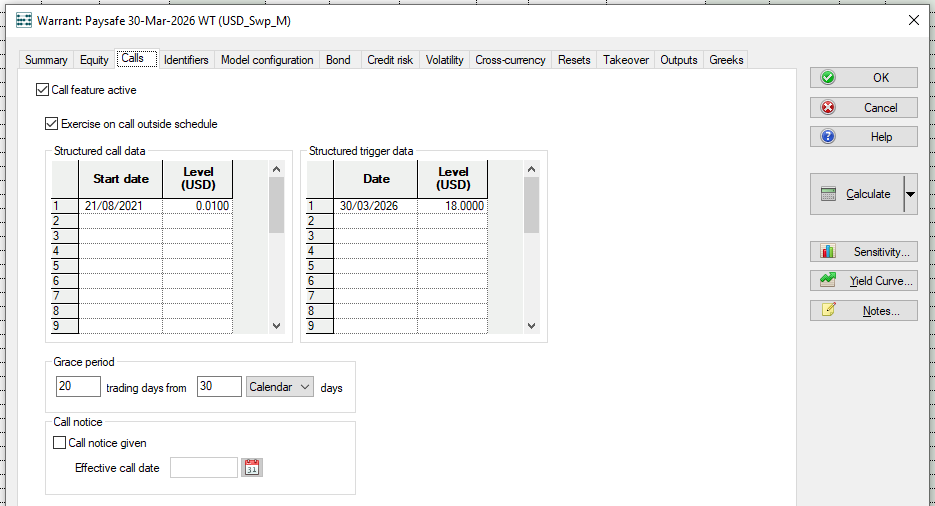

The SPAC lists on a stock exchange in order to raise money from investors who typically pay $10 per "unit", consisting of an ordinary share and an option to buy more shares later via warrants. The SPAC has a limited amount of time (typically two years) in which to complete a successful acquisition, or Initial Business Combination (IBC), after which the warrants become exercisable. A key difference from traditional warrants, SPAC warrants may be redeemed by the issuer once the shares exceed a trigger price, the issuer soft-call. In Monis we have extended our warrant model to include a soft-call feature and allow SPAC warrants to be modelled more accurately.

Early redemption

The soft-call is typically for a minimal cash amount (e.g. $0.01 per warrant) and exists in order to force a holder to exercise once the share price reaches $18, typically. Roughly half of the SPAC warrants issued during the last 18 months have also included a second soft-call, with a $10 trigger. Both calls are active throughout the life of the instrument. We shall refer to these as the "$18 triggered call" and the "$10 triggered call", where these cash amounts refer to the calls’ share price trigger level.

The $18 triggered call exists to force exercise when the stock price performs well, and the exercise is defined as per the usual exercise rights available to the holder. The $10 triggered call is more complex. In this case the warrants are exercised on a cashless basis – holders pay no exercise price, but instead surrender their warrants for a fraction of the shares they would have received. A pre-defined table of share prices and remaining time to maturity is used to determine the number of shares holders receive (rather like the make-whole replacement shares table for a convertible instrument). Forcing holders to exercise on a cashless basis would allow the company to avoid the higher level of dilution a full exercise would result in, but at the expense of foregoing any additional capital injection.

SPAC Warrant case study

We will consider an example of a SPAC warrant with summary terms as per below.

5-Year Maturity

$11.50 Exercise Price (strike)

European Exercise (with exercise on call)

Lifetime Call for $0.01 with a $18 trigger, with regular exercise

Lifetime Call for $0.10 with a $10 trigger, with cashless exercise

Risk Free Rate 3%

The $10 triggered call, or cashless exercise call, has a payoff as defined by the below table, where the lookup is done based upon the current share price and months until the maturity date. The value in the table represents the number of shares per warrant received upon exercise. The values used in these tables are almost entirely generic across all SPAC warrant instruments featuring the cashless exercise call.

Modelling the calls

The below chart shows the impact on valuations of modelling the $10 triggered call in addition to the $18 triggered call, using a fixed $10 spot price. The $10 triggered call has minimal impact for volatilities below 40%, yet has a clear capping effect thereafter, which is not present when only the $18 triggered call is considered. It would therefore be prudent, in the absence of explicitly modelling the $10 call, to cap user input volatility assumptions at around 40% for instruments with this feature, even where realised volatility is much higher.

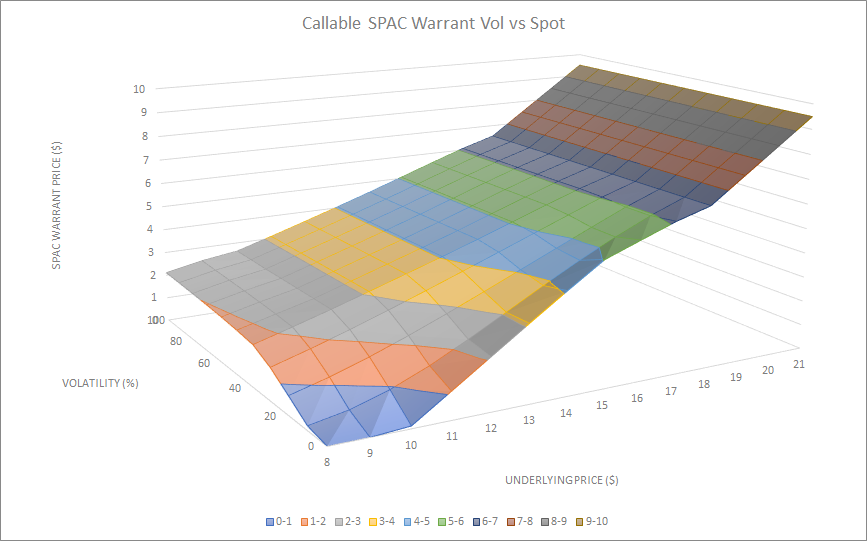

Varying volatility and spot price for the warrant with both the $18 and $10 triggered calls active produces the valuation surface, illustrated below. Volatility (%) is assumed flat over the instrument lifetime and the spot price ranges from $8 up to a maximum of $21. Above the $18 spot we observe the expected behaviour whereby the fair value is given simply by the spot minus the strike, represented by the perfectly flat plane we see above $18 spot, irrespective of the volatility assumptions. Also of interest is the flat plane we see above approximately 40% volatility for all spot prices. This corresponds to the capped region in the previous graph and is the impact observed as a direct result of the $10 triggered call.

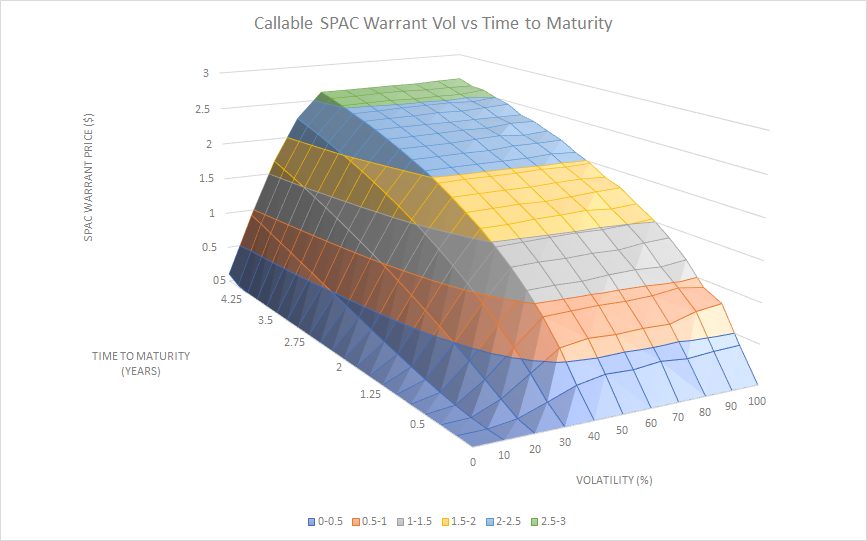

The final surface below looks at the valuation profile of the SPAC warrant with both calls active as we reduce the time to maturity (three months at a time), varying volatility and using a constant spot price of $10. As expected, throughout the instrument's lifetime, we continue to see this capping effect of the $10 triggered call above approximately 40% volatility.

Further research

The flat region we observe in the valuation surface, above approximately 40% volatility, leads to a strongly concave relationship between price and volatility. This suggests that a stochastic volatility model may be an important further area of research when analysing the negative impact of the $10 triggered call. In our example we have not attempted to capture some of the more subtle features of the cashless exercise payoff which could be of interest, especially in high volatility environments where the $10 call would appear to impinge most on valuations. One such subtlety is that the share price lookup used in the cashless exercise table is often determined using an n-day average or volume weighted price, making the payoff path dependent and the warant's relationship with volatility even more complex. Another such detail is the period between the call notice being given by the issuer and the effective call date, on which the exchange of warrants for shares occurs, which makes the forced exercise akin to a compound option which we would expect to add some additional value.

Modelling SPAC Warrants in Monis

The latest release of the Monis Analytics now incorporates the ability to model a soft-call feature for the warrant instrument. For SPAC warrants where both the $18 and $10 calls exist we believe the results of our analysis demonstrate the validity in modelling the $18 triggered soft-call whilst capping the input vol assumption at a maximum 40% as a proxy for the impact of the $10 triggered forced cashless exercise.

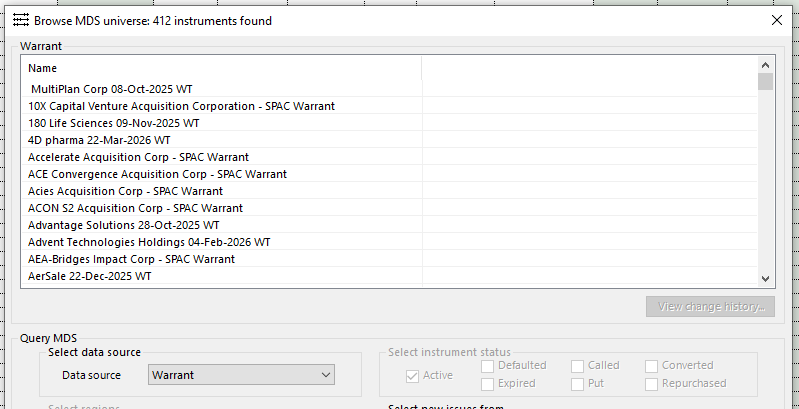

The Monis Data Service has been extended to provide and maintain the terms and conditions data for the SPAC warrants universe. Warrants for those SPACs that are in their pre-acquisition stage of life are modelled using their rolling (typically 5 year) maturity. Once the merger is complete, terms are updated to their known fixed dates.

Contact us

If you would like to discuss this, or any other aspect of Monis or the Data Service, please feel free to contact us at Monis support.

philip.kramer@fisglobal.com

tatyana.hube@fisglobal.com

william.weichhart@fisglobal.com

monis.data@fisglobal.com

With special thanks to Rhory Ashworth for his contribution to this report.

Copyright © 2021 by Fidelity National Information Services, Inc. and/or its subsidiaries ("FIS"). This document is copyrighted with all rights reserved. No part of this document may be reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of FIS. Except as set out in the contract your company has with FIS, in no event shall FIS be liable for damages of any kind arising out of the use of this document.